Executive Summary

This section should concisely convey the core value, technological features, problems addressed, and target market of the AI-driven quantitative trading system, using precise and clear language for a high-level summary.

1. Project Overview

In the context of increasingly complex global financial markets dominated by high-frequency trading (HFT), traditional trading strategies are often constrained by limitations in data processing, decision speed, and market adaptability. This project aims to develop an AI-driven quantitative trading system that leverages machine learning, deep reinforcement learning, natural language processing (NLP), and high-frequency trading algorithms to provide precise, automated, and low-latency smart trading solutions for institutional investors, hedge funds, and individual traders. The system is powered by Visionary Profit System 6.0, integrating big data analytics, AI predictive modeling, and real-time trade execution, offering sustainable and optimized quantitative trading strategies to improve trading efficiency and enhance risk management.

2. Key Technical Features

The core technical features of the system include:

-

AI-Driven Trading Signal Generation

- Leverages deep learning (LSTM, Transformer) and reinforcement learning (PPO, DDPG) to predict market trends.

-

Market Sentiment Analysis

- Integrates social media and news sentiment analysis (NLP) for market sentiment modeling to optimize trading strategies.

-

Adaptive Quantitative Trading Strategies

- Combines statistical arbitrage, trend-following, and HFT strategies for dynamic optimization.

- Visionary Profit System 6.0 enables AI trading models to adjust parameters in real-time to adapt to market fluctuations.

-

High-Speed Execution & Risk Management

- Low-latency algorithmic trading (HFT) enabled by distributed computing and FPGA acceleration for millisecond-level execution.

- Built-in multi-layer risk management system, including real-time value-at-risk (VaR) and black swan event detection.

-

Comprehensive Data Integration & Analysis

- Integrates market data, order flow, macroeconomic data, news, and social media sentiment.

- Uses real-time data streaming (Kafka) and big data storage (Hadoop, Snowflake) for efficient data processing.

-

Scalable Architecture & API Integration

- Utilizes microservices architecture (Kubernetes, Docker) for scalability and high availability.

- Provides API interfaces for integration with exchanges, financial institutions, and third-party data sources.

3. Core Problems Addressed

-

Latency in Trading Signals & Low Accuracy

- Traditional technologies struggle with efficiently processing large volumes of data, leading to delayed signals and inaccurate trading decisions.

- Visionary Profit System 6.0 uses deep reinforcement learning and HFT to adapt in real-time, improving signal accuracy.

-

Insufficient Market Sentiment Analysis

- Traditional quantitative models fail to fully leverage unstructured data such as news and social media.

- This system integrates NLP and large-scale market sentiment analysis to enhance market forecasting ability.

-

Inefficiency in Strategy Execution & High Trading Costs

- Order execution delays and slippage impact profitability, and traditional models struggle to optimize execution paths.

- The system uses smart order splitting and dynamic arbitrage optimization to reduce trading costs.

-

Inadequate Risk Management Systems

- Traditional risk management relies on static indicators and lacks dynamic responses to extreme market events.

- The system integrates AI-driven risk modeling, anomaly detection, and real-time stop-loss mechanisms to enhance risk control capabilities.

4. Target Audience & Market Positioning

The primary target audience for this system includes:

- Institutional Investors

- Hedge Funds

- Asset Management Firms

- Proprietary Trading Firms

- Retail Traders & High-Net-Worth Individuals

- Quantitative Trading Enthusiasts

- Institutional Traders

- Fintech Platforms & Exchanges

- Stock Exchanges (NYSE, NASDAQ, LSE, etc.)

- Cryptocurrency Exchanges (Binance, Coinbase, OKX)

- Brokerages (Interactive Brokers, TD Ameritrade)

Market Positioning:

- High-frequency trading (HFT) smart solution provider.

- AI-powered intelligent quantitative trading platform.

- Full-stack trading strategy solutions (from data to execution).

Background & Industry Landscape

This chapter aims to provide readers with an understanding of the background of quantitative trading, highlight the application trends of AI technology, and delve into the regulatory environment of the financial industry. Through this chapter, readers will understand the market environment, existing challenges, and potential of AI-driven quantitative trading systems.

1. Challenges Facing Traditional Quantitative Trading

Traditional quantitative trading relies on mathematical models, statistical analysis, and computer algorithms to identify arbitrage opportunities in the market. However, with changing market conditions and the exponential growth of data, traditional quantitative trading faces several major challenges:

-

High Dimensionality and Complexity of Data

- Traditional quantitative trading typically relies on structured financial data (such as stock prices, historical data, etc.), but unstructured data in the market (such as news, social media, industry reports, etc.) has not been effectively utilized.

- The volume and dimensionality of market data are growing exponentially, and traditional systems face significant bottlenecks when processing large amounts of data.

-

Model Adaptability and Stability

- Traditional models are often based on fixed rules and statistical methods and lack flexibility to adapt to changing market conditions.

- In extreme market fluctuations or black swan events, traditional quantitative strategies often perform poorly, potentially leading to significant losses.

-

Inefficient Execution and High Costs

- Particularly in high-frequency trading (HFT), delays between signal generation and execution can significantly increase trading costs.

- Slippage and trading costs are difficult to optimize in traditional systems, affecting the overall performance of strategies.

-

Insufficient Risk Management

- Traditional risk control models often rely on historical data and static models, making them inadequate for responding to dynamic market changes and lacking sensitivity to risks.

- Many traditional quantitative models fail to account for extreme risks, such as black swan events, and thus cannot effectively avoid unforeseen market risks.

2. AI Applications in Financial Markets

With the increase in computing power and continuous advancements in AI technology, the use of AI in the financial industry is rapidly expanding, especially in the field of quantitative trading. AI technologies are gradually replacing traditional models, providing smarter and more flexible trading solutions. Major AI applications in financial markets include:

-

Intelligent Trading Signal Generation

- AI, through deep learning, reinforcement learning, and other algorithms, is able to predict market movements and generate more accurate trading signals based on big data (historical data, real-time data, news, and social media sentiment).

- Compared to traditional methods, AI can capture more complex market dynamics and potential nonlinear relationships, offering more precise buy/sell decisions.

-

Algorithm Optimization & Adaptive Trading

- Based on reinforcement learning, AI models can automatically adjust trading strategies to adapt to constantly changing markets. For example, deep Q-learning (DQN) can optimize trading decisions, improving the stability and profitability of strategies.

- AI can self-adapt to adjust parameters and optimize strategies in dynamic market environments.

-

Big Data & Sentiment Analysis

- AI can extract sentiment information from unstructured data (such as news, earnings reports, social media) to provide additional signals for the market.

- Through natural language processing (NLP), AI can perform sentiment analysis to help trading systems better understand shifts in market sentiment and capture small market fluctuations ahead of time.

-

High-Frequency Trading & Low-Latency Execution

- AI, combined with HFT technology, can make trading decisions at millisecond speeds, significantly increasing trading efficiency.

- Through quantitative algorithms and low-latency network architecture, AI can reduce execution delays and slippage, thus significantly lowering trading costs.

-

Intelligent Risk Management

- AI can perform dynamic risk monitoring based on real-time data streams, machine learning models, and extreme market condition simulations.

- During market volatility or sudden events, AI systems can automatically trigger stop-loss orders or adjust risk exposure to maintain portfolio stability.

3. Regulatory Environment Analysis

The regulatory environment of the financial market plays a critical role in the implementation of smart quantitative trading systems. Governments and financial regulators across the globe are formulating policies and laws to regulate the use of AI technology, ensuring its development within a legal and compliant framework. Current regulatory trends include:

-

Tightening Global Financial Regulations

- With the rapid development of AI and algorithmic trading, regulatory agencies are enhancing their oversight of quantitative trading and AI applications. For example, the EU's MiFID II regulation sets strict requirements for algorithmic trading and market transparency.

- Regulatory agencies like the U.S. SEC are gradually updating their requirements for algorithmic trading and AI systems to ensure fairness and transparency in financial markets.

-

AI Ethics & Compliance Issues

- As AI becomes widely used in finance, regulators require AI models to be transparent and interpretable, avoiding "black box" operations.

- Regulators are also concerned with potential discriminatory biases in AI systems, especially in areas like credit, loans, and investment decisions, ensuring fairness when processing data.

-

Market Manipulation & Abuse Prevention

- Regulatory agencies are highly concerned with potential market manipulation brought by AI algorithms (e.g., false trades, price manipulation) and require all trading algorithms to comply with regulations and include audit and regulatory tracking capabilities.

- For instance, the CFTC in the U.S. has increased efforts to combat market manipulation through algorithmic trading.

-

Data Privacy & Protection

- Since AI systems rely on big data, user privacy protection is a critical issue.

- Regulations such as the General Data Protection Regulation (GDPR) require financial institutions to ensure the security and privacy of user data within AI models, preventing data leaks and misuse.

-

Intelligent Risk Management

- AI can perform dynamic risk monitoring based on real-time data streams, machine learning models, and extreme market condition simulations.

- During market volatility or sudden events, AI systems can automatically trigger stop-loss orders or adjust risk exposure to maintain portfolio stability.

System Architecture

This section provides an overview of the overall structure of the AI-driven quantitative trading system, detailing the core components, technology stack, and development framework to ensure the reader understands the system's architecture and its technical implementation.

1. Overall Architecture Design

The system adopts a layered architecture model, where each layer has a specific function, ensuring high scalability, availability, and performance:

Data Layer

-

Function

- Responsible for collecting and storing raw data from various data sources, ensuring real-time updates and efficient retrieval.

-

Data Sources

- Market Data: Stock, Forex, cryptocurrency prices, and exchange data (e.g., Binance, Coinbase).

- Unstructured Data: News, social media, earnings reports, etc., using Natural Language Processing (NLP) for sentiment analysis and information extraction.

- Historical and Real-Time Data: Includes candlestick data, order books, trading volume, etc.

-

Technical Tools

- Kafka: Used for real-time data stream processing, ensuring low-latency data transmission.

- Hadoop/Spark: Used for large-scale data storage and processing, supporting efficient data analysis.

- Redis: Used for real-time caching, speeding up data retrieval.

Model Layer

-

Function

- Deeply analyzes and models the data to generate trading signals and optimize trading strategies.

-

Key Tasks

- Factor Analysis: Extracts market-relevant features such as momentum, volatility, etc.

- Machine Learning Models: Uses deep learning and reinforcement learning algorithms for model training.

- Risk Prediction: Predicts potential market risks and adjusts strategies accordingly.

-

Technical Tools

- TensorFlow/PyTorch: For training deep learning models, supporting GPU acceleration.

- Scikit-learn, XGBoost: For traditional machine learning models.

- NLP Models (e.g., BERT): Used for processing unstructured data like news and social media.

Execution Layer

-

Function

- Converts the trading signals generated by the model into market orders, executes trades, and provides real-time feedback.

-

Key Tasks

- Smart Order Execution: Optimizes order execution paths, reducing slippage and transaction costs.

- Order Routing: Routes orders to appropriate exchanges for optimal execution.

- Execution Strategy Optimization: Adjusts execution strategies in real-time based on market conditions.

-

Technical Tools

- FIX Protocol: Used for high-frequency trading and fast communication with exchanges.

- Exchange APIs (e.g., Binance, Kraken): For executing actual orders.

- Order Book Management: Monitors the order book in real-time to optimize trading decisions.

Overall Architecture Diagram

The architecture uses a layered structure (Data Layer, Model Layer, Execution Layer), with arrows indicating the flow of data. Integration and communication between layers occur through APIs and message queues (e.g., Kafka).

2. Core Components

Data Processing

-

Data Collection and Cleaning: Ensures data quality by cleaning, denoising, and filling missing values to optimize the data.

- Tools: Pandas, NumPy for data preprocessing.

- Kafka: For real-time data collection and transmission.

Factor Analysis

-

Function: Extracts factors from market data using statistical methods and machine learning for building trading strategies.

- Tools: Pandas, NumPy for factor computation, Scikit-learn, XGBoost for modeling.

Model Training

-

Function: Uses deep learning and reinforcement learning to train models, predict market trends, and generate trading signals.

- Tools: TensorFlow, PyTorch for deep learning models; Keras, Gym for reinforcement learning training.

Trade Execution

-

Function: Generates and executes orders based on trading signals. The smart trading engine reduces market impact, slippage, and transaction costs by splitting orders and routing them optimally.

- Tools: FIX Protocol for communication with exchanges, Redis for caching order data to reduce response time.

Risk Management

-

Function: Monitors market conditions and trade risks in real-time, ensuring trades remain within risk limits and triggering stop-loss strategies when necessary.

- Tools: NumPy, SciPy for calculating risk indicators such as VaR (Value-at-Risk) and CVaR (Conditional VaR); TensorFlow, PyTorch for training risk prediction models.

3. Technology Stack and Development Framework

This system is built on Python, integrating advanced machine learning, distributed computing, and real-time data processing technologies to ensure efficient performance and scalability:

Programming Language

- Python: Widely used in quantitative trading and machine learning, supporting libraries for data analysis, machine learning, and deep learning.

Machine Learning and Deep Learning Frameworks

- TensorFlow/PyTorch: For building and training trading models using deep learning frameworks.

- Scikit-learn, XGBoost: For traditional machine learning models used in factor analysis and regression models.

Real-Time Data Streaming and Distributed Computing

- Kafka: For real-time data stream processing.

- Hadoop/Spark: For large-scale data storage and processing, ensuring efficient data analysis.

- Redis: Real-time caching technology to reduce database query latency.

Trade Execution and Order Management

- FIX Protocol: For high-frequency trading and fast communication with exchanges.

- RESTful APIs: For integration with financial exchanges.

Cloud Computing and Deployment

- AWS/GCP: Cloud platforms for model training, data storage, and deployment.

- Kubernetes/Docker: For containerized deployment and microservice management.

Other Tools

- Jupyter: For data analysis and model development.

- Git: Version control tool to ensure efficient collaboration among the development team.

AI Trading Model

This chapter provides an in-depth look at the core components of the AI-driven quantitative trading system: the AI trading model. The focus is on data acquisition and preprocessing, trading signal generation, optimization algorithms and backtesting, and model interpretability, all of which provide strong support for the system and ensure the reliability of the final trading decisions.

1. Data Acquisition and Preprocessing

The quality and processing of data form the foundation of the AI trading model, directly influencing the model's performance. This section covers data source selection, data cleaning, and feature engineering.

Data Sources

- Market Data: Includes historical prices, trading volumes, and volatility for financial products like stocks, forex, futures, and cryptocurrencies. Data comes from exchanges (e.g., Binance, Coinbase, NASDAQ) and financial websites (e.g., Yahoo Finance, Bloomberg).

- Unstructured Data: Includes news articles, social media content, financial reports, macroeconomic indicators, etc. NLP techniques are used to analyze text data and extract market sentiment information.

- Economic Data: Data like GDP, interest rates, inflation, and unemployment rates helps identify long-term market trends.

Data Cleaning

- Noise Removal: Techniques like outlier removal, missing value imputation, and data smoothing ensure data reliability. Outliers are detected and handled using methods such as Z-Score or IQR.

- Data Standardization: Standardization or normalization techniques are used to ensure consistent feature scales, preventing certain features from dominating model training.

Feature Engineering

- Factor Extraction: Generates features using technical indicators (e.g., RSI, MACD, Bollinger Bands) and fundamental metrics (e.g., P/E ratio, debt-to-equity ratio). Combining time-series features and market sentiment (e.g., news sentiment, social media data) helps create new features.

- Principal Component Analysis (PCA): A dimensionality reduction method that removes redundant features and retains the most important factors, improving training efficiency.

2. Trading Signal Generation

Trading signal generation is one of the core tasks of the AI trading model, aimed at generating buy, sell, or hold signals based on market data. AI models typically use various machine learning techniques to generate signals, including supervised learning, reinforcement learning, and deep learning.

Supervised Learning

- Regression and Classification Models: Regression models (e.g., linear regression, SVR) are used to predict price movements and generate trading signals. Classification models (e.g., decision trees, SVM, logistic regression) are used to identify market states (e.g., uptrend, downtrend, consolidation) and generate buy/sell signals.

Reinforcement Learning

- Reinforcement Learning Concept: Reinforcement learning models guide behavior selection through agent-environment interactions using reward signals, progressively optimizing trading strategies. Common algorithms include Deep Q-Learning (DQN), Proximal Policy Optimization (PPO), and Policy Gradient methods.

Deep Learning

- Neural Network Models: Long Short-Term Memory (LSTM) networks and other Recurrent Neural Networks (RNN) are used for time-series data, capturing long-term and short-term dependencies in market trends. Convolutional Neural Networks (CNN) process multi-dimensional data (e.g., candlestick charts), while Transformer models capture long-range dependencies to improve signal prediction accuracy.

3. Optimization and Backtesting

To improve the stability and accuracy of the trading model, optimization algorithms and backtesting systems are employed to adjust and validate model parameters, ensuring the model adapts to real-world market conditions.

Monte Carlo Simulation

- Function: Generates a large number of market scenarios through random simulations to assess model performance under various market conditions and test its robustness.

Bayesian Optimization

- Function: Uses Bayesian methods to optimize model hyperparameters, reducing computation time compared to traditional methods (e.g., grid search, random search). Gaussian processes estimate function distributions and adjust hyperparameters for optimal performance.

Genetic Algorithm

- Function: Based on natural selection principles, genetic algorithms optimize trading strategies through selection, crossover, and mutation operations. They are particularly effective in multi-objective optimization in high-dimensional spaces.

Backtesting

- Function: Validates model effectiveness using historical market data. Performance metrics (e.g., maximum drawdown, annualized return, Sharpe ratio) are used to evaluate the strategy. Overfitting detection ensures that the model performs well on both historical data and real-time market conditions.

4. Model Interpretability

With AI's growing role in finance, model interpretability has become increasingly important. Regulatory requirements and investor demands call for transparency and understanding of AI model decision-making processes.

SHAP (SHapley Additive Explanations)

- Function: SHAP is a method for assigning feature contribution values, helping to understand why a model made a particular prediction. Based on Shapley value theory, SHAP provides high precision by assigning contribution values to each feature, explaining the model's decision-making process.

LIME (Local Interpretable Model-agnostic Explanations)

- Function: LIME is a local interpretability method that fits a simpler model to explain the behavior of complex models for specific inputs, helping investors understand the model's response to specific data points.

Importance of Model Interpretability

- Regulatory Requirements: Regulators require AI systems to have transparency and fairness, ensuring financial decisions are not influenced by "black-box" effects.

- Investor Trust: Enhancing model interpretability helps build trust with investors, encouraging greater market participation.

Trade Execution and Risk Management

Trade execution and risk management are core components of quantitative trading systems, directly affecting the effectiveness of trading strategies and the safety of investments. This chapter will provide a detailed explanation of smart execution engines, real-time risk management systems, and anomaly detection and automated handling, which form the foundation for ensuring efficient execution and effective risk control.

1. Smart Execution Engine

The smart execution engine is one of the key components of a quantitative trading system, ensuring the efficient execution of trading strategies while minimizing market impact and transaction costs.

High-Frequency Trading (HFT)

- High-frequency trading leverages ultra-low latency and high transaction volume. The system uses advanced algorithms and high-speed trading infrastructure to capture short-term market opportunities.

- The trading system analyzes market data at the microsecond level and executes orders instantly, responding quickly to market fluctuations to capture profits from small market movements.

- Parallel computing and low-latency network optimization enhance trading speed, ensuring a competitive advantage in exchange pairing systems.

Algorithmic Trading

-

Algorithmic trading automatically executes trades based on pre-set rules and strategies, without the need for manual intervention. Common algorithms include:

- VWAP (Volume Weighted Average Price): Distributes orders evenly to minimize market impact.

- TWAP (Time Weighted Average Price): Distributes orders evenly across a specified time period to reduce market impact.

- Iceberg Orders: Breaks large orders into smaller orders to avoid market attention.

- Strategy Optimization: Machine learning algorithms, such as reinforcement learning, are used to continuously optimize trading strategies, improving execution efficiency and minimizing costs.

Order Management

- Order Routing System (OMS): Automatically selects the best exchange or broker for order execution to reduce trading costs.

- Transaction Cost Analysis (TCA): Assesses the cost of trade execution, helping evaluate the efficiency of algorithms and make adjustments based on feedback.

- Order Allocation Strategy: Adjusts the order allocation method based on market conditions to ensure that large transactions have minimal market impact.

2. Real-Time Risk Management System

Risk management is an essential part of a quantitative trading system, ensuring that trading strategies comply with preset risk limits and preventing significant losses from market fluctuations or system failures.

VaR (Value at Risk)

- VaR is a common method for measuring potential risks, calculating the maximum possible loss within a specified time frame and confidence level.

- The VaR model uses statistical analysis of historical data to simulate the impact of market price fluctuations on a portfolio, helping assess the potential range of maximum losses.

- VaR can be calculated for different time frames (e.g., daily, weekly, monthly) and confidence levels (e.g., 99%, 95%).

CVaR (Conditional Value at Risk)

- CVaR is an extension of VaR, focusing on evaluating losses beyond the VaR threshold, considering extreme market events.

- It measures tail risks beyond the VaR point, assessing potential losses due to extreme market fluctuations at specific confidence levels.

Markov Process

- The Markov process is used to predict market state transitions, utilizing a state transition matrix to evaluate the probability of different market states.

- By analyzing past market behavior patterns, it helps predict future price fluctuations and manage market volatility and potential risks.

- In practice, the Markov process is widely used in asset pricing models and risk exposure forecasting.

Risk Budgeting

- Risk budgeting allocates risk contributions among different assets to control overall risk levels, ensuring that each trading strategy's risk exposure does not exceed preset thresholds.

- Risk weights are assigned to sub-strategies and assets using metrics like VaR or CVaR.

3. Anomaly Detection and Automated Handling

To ensure the stability of the trading system and prevent losses due to market anomalies, technical failures, or malicious attacks, the system must continuously monitor and identify potential abnormal behaviors.

Anomaly Detection

-

Statistical Methods: Builds statistical models of normal market behavior to identify anomalies significantly different from historical data (e.g., sudden price surges or abnormal trading volumes).

- For example, Z-Score or IQR methods can be used to detect price fluctuations that fall outside of reasonable ranges.

-

Machine Learning Methods: Unsupervised learning techniques, such as autoencoders or isolation forests, are used to train data and identify abnormal patterns.

- Deep learning models, such as LSTM, can also monitor abnormal fluctuations in time series data.

Real-Time Monitoring and Alerts

- Real-Time Data Streaming Systems (e.g., Apache Kafka): Analyzes market data in real time, automatically detecting anomalies and sending risk alerts.

- Threshold Settings: Different alert levels are set based on market conditions, triggering specific actions (e.g., halting trading, limiting maximum trade volume).

Automated Handling

- Automated Trade Suspension: When the system detects market anomalies, it automatically triggers a trade suspension to prevent further losses.

- Automated Position Adjustment: Based on real-time risk feedback, the system can automatically adjust positions to reduce exposure.

- Strategy Replacement: In the event of an anomaly, the system can automatically switch to a low-risk strategy based on preset rules.

Anomaly Reporting and Auditing

- The system generates anomaly reports for risk control personnel to review and analyze afterward.

- Audit Logs: All trade executions and risk control decisions are recorded to ensure compliance and traceability.

Performance Evaluation and Optimization

In a quantitative trading system, performance evaluation and optimization are key steps in ensuring the long-term stability and effectiveness of models and strategies. Through an effective backtesting framework, performance metrics, and dynamic adaptive optimization strategies, we can gain a deep understanding of the actual performance of trading strategies and adjust and improve them based on evaluation results. This chapter will elaborate on these important aspects, helping systems evolve continuously to achieve the best investment outcomes.

1. Backtesting Framework

Backtesting is a fundamental tool for validating the effectiveness of trading strategies. It tests a strategy's historical performance by simulating past market conditions, providing the basis for further optimization.

- Historical Backtesting

Historical backtesting involves applying a strategy to historical data to simulate its performance under past market conditions.

This method assesses the strategy's stability by testing its performance under various market conditions (such as bull markets, bear markets, and sideways markets), providing a clear understanding of the strategy's behavior.

During the backtest, ensuring the completeness and accuracy of data is critical to avoid future result bias.

- Hypothesis Testing

Hypothesis testing is used to validate a strategy's effectiveness. For example, the t-test is used to determine if the strategy's returns are significantly higher than market benchmarks or random strategies.

Common hypothesis tests compare the null hypothesis (an ineffective strategy) with the alternative hypothesis (an effective strategy), using p-values and confidence intervals to assess the reliability of the strategy.

Hypothesis testing in backtesting also helps evaluate the strategy's robustness and generalizability to prevent overfitting.

- Transaction Cost Analysis (TCA)

Transaction costs play an important role in quantitative trading, especially in high-frequency trading strategies. These include:

Explicit Costs: Such as commissions, slippage, and taxes.

Implicit Costs: Such as market impact and liquidity risk.

The TCA framework quantifies these costs and evaluates the strategy's actual returns relative to its cost impact.

By optimizing order execution algorithms, slippage and market impact can be reduced, improving the net returns of the strategy.

2. Performance Metrics

To evaluate trading strategies, multiple performance metrics are used to assess the risk-adjusted returns, stability, and sustainability of strategies.

- Sharpe Ratio

The Sharpe ratio measures excess return per unit of risk and is calculated as:

Where:

σp is the strategy's annualized return,

A higher Sharpe ratio indicates better risk-adjusted returns, allowing investors to obtain higher returns for the same level of risk.

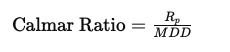

- Calmar Ratio

The Calmar ratio evaluates a strategy's performance during the maximum drawdown period and is calculated as:

Where:

Rp is the annualized return,

MDD is the maximum drawdown.

A higher Calmar ratio indicates that the strategy can generate good returns even during periods of maximum drawdown, making it suitable for evaluating a strategy's ability to withstand risk.

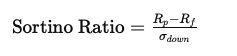

- Sortino Ratio

The Sortino ratio is an improvement of the Sharpe ratio, focusing specifically on downside volatility and is calculated as:

Where:

Rp is the annualized return,

Rf is the risk-free rate,

σdown is the standard deviation of negative returns.

A higher Sortino ratio indicates that the strategy has achieved good returns while managing downside risk.

- Maximum Drawdown (MDD)

Maximum drawdown measures the largest loss over a specific period, providing an indication of the strategy's risk.

By analyzing MDD, investors can assess the potential range of capital fluctuations, helping them adjust the risk exposure in their portfolio.

3. Dynamic Adaptive Optimization Strategies

As market conditions change, quantitative trading strategies must have the ability to adapt in real-time. Dynamic adjustments based on real-time data and market volatility help maximize profits and minimize risks.

- Dynamic Parameter Adjustment

During trading, the parameters of the strategy may need to be adjusted dynamically based on market volatility, liquidity, or other market conditions.

Adaptive algorithms (such as genetic algorithms or Bayesian optimization) continuously update strategy parameters based on new data, ensuring the strategy remains in its optimal state.

- Rolling Backtesting

Rolling backtesting divides data into training and testing sets, using the latest market data to retrain the model and validate its effectiveness on new datasets.

By regularly retraining and optimizing the model, rolling backtesting ensures that the strategy adapts to changing market conditions.

- Online Learning

Online learning is a machine learning method that allows the model to adjust as new data enters in real-time without retraining the entire dataset.

Online learning can quickly respond to market changes, providing flexible strategy updates and ensuring that the trading system remains synchronized with dynamic market conditions.

- Dynamic Risk Adjustment

In highly volatile or extreme market conditions, strategies will dynamically reduce risk exposure or modify risk management rules to avoid significant losses.

Risk control models trigger real-time adjustments, such as stop losses, take profits, or position adjustments, to prevent the accumulation of risk.

Compliance and Security

In the financial markets, compliance and security are core components of the design and operation of quantitative trading systems. With the widespread use of artificial intelligence (AI), regulatory authorities are increasingly demanding compliance and transparency. This chapter explores international and local regulatory requirements, AI transparency and ethical issues, as well as data security and privacy protection to ensure trading systems comply with regulations while maximizing protection for investors and users.

1. International and Local Regulatory Requirements

The compliance requirements for quantitative trading systems are governed by regulations set by financial regulatory bodies worldwide. Different regions have different regulatory frameworks, and compliance ensures legal adherence while enhancing trust among market participants.

-

U.S. Securities and Exchange Commission (SEC)

The SEC regulates trading activities in U.S. securities markets to ensure fairness, transparency, and efficiency. For quantitative trading systems, the SEC mandates:

- Transparent Trading and Reporting: All trading activities must be reported to regulators as required.

- Anti-Fraud Rules: Market manipulation and unfair practices are prohibited, and quantitative trading systems must adhere to laws regarding insider trading and market manipulation.

- Algorithmic Trading Regulation: The SEC requires monitoring of high-frequency trading and automated trading strategies to ensure they do not overly impact the market.

-

MiFID II (Markets in Financial Instruments Directive II)

MiFID II is one of the primary legal frameworks regulating financial markets in the EU, requiring that all financial services and trading activities follow principles of transparency, fairness, and efficiency. Key components include:

- Algorithmic Trading Regulation: Stricter regulations on automated trading systems, requiring detailed reporting.

- Market Transparency: Mandates disclosure of market information, especially related to large trades, price transparency, and financial instruments.

- Risk Management and Compliance Audits: Requires financial institutions to establish compliance review procedures to ensure trading activities align with regulatory standards and prevent market risk accumulation.

-

China Securities Regulatory Commission (CSRC)

The CSRC regulates quantitative trading systems in China, with key regulations including:

- Trading Behavior Compliance: Requires strict review of trading activities to ensure they meet legal standards and prevent insider trading and malicious practices.

- System Registration and Regulation: Quantitative trading systems must undergo a registration process to ensure their legality.

- Market Fairness and Transparency: The CSRC emphasizes market fairness and requires trading platforms and systems to maintain transparency to prevent improper market manipulation through algorithms.

2. AI Transparency and Ethical Issues

With the widespread use of artificial intelligence in financial markets, AI system transparency and ethical issues have become significant concerns. Ensuring AI systems adhere to ethical standards is not only a legal requirement but also a key factor in maintaining trust among users and market participants.

-

AI Transparency

- Explainability: AI decision-making transparency requires that its decision-making process is understandable, especially when financial decisions are involved. Explainability techniques such as SHAP and LIME help provide an explanation of the model's decision-making process.

- Model Auditing: AI models should be audited regularly to check for potential biases or non-compliant behaviors. Transparent auditing processes help build market trust and ensure decisions align with ethical standards.

- Data Traceability: Ensuring transparency in data sources, usage, and purposes is crucial. The system should maintain complete data lifecycle records to facilitate regulatory reviews.

- AI Ethical Issues

- Fairness and Non-Discrimination: AI systems should process data and make decisions impartially, preventing unfair impacts on certain groups or individuals. Algorithms must avoid discriminatory decisions, especially in areas like credit scoring and investment advice.

- Accountability for Automated Decisions: It must be clear who is responsible for the results of automated decisions. If AI systems make errors or cause losses, there should be a clear accountability mechanism.

- Client Privacy and Interests Protection: AI must adhere to privacy standards, ensuring that customer data is not misused or improperly analyzed.

3. Data Security and Privacy Protection Financial trading systems process large volumes of sensitive information, including client personal data, investment portfolios, and transaction history. Ensuring data security and privacy protection is a vital component of compliance.

- Data Encryption

Data transmission and storage should use encryption technologies like SSL/TLS to protect sensitive information from unauthorized access.

Data encryption is essential to prevent cyberattacks, such as man-in-the-middle attacks, and ensure that client data remains private and secure.

- Data Anonymization

Data anonymization involves removing personal identifiers from data before it is processed or analyzed. This technique minimizes the risk of privacy violations while enabling data analysis without compromising individual privacy.

Anonymizing sensitive data before sharing or using it helps ensure compliance with data privacy regulations.

- Regulation Compliance

- Data Retention Policies: Data retention requirements may mandate that trading platforms retain client data for a set period, but this data must also be protected during that time.

- Incident Response Plans: In the event of a data breach, financial institutions must have incident response plans in place to mitigate damage and protect users.

In addition to general data protection laws like GDPR in Europe and CCPA in California, financial institutions must also comply with industry-specific data protection regulations. These include:

Business Model and Application Scenarios

The business model and application scenarios of quantitative trading systems cover a wide range of investor groups, providing comprehensive solutions for institutional investors as well as individual investors. This chapter will explore how different user groups can improve investment outcomes through this system and demonstrate its diverse commercial value in practical applications. By catering to institutional investors, retail investors, and integrating with SaaS solutions via APIs, the quantitative trading system offers personalized and flexible services to participants in the financial markets.

1. Institutional Investors

Institutional investors, such as hedge funds, banks, and asset management companies, typically have more complex investment needs and larger capital scales, requiring higher system performance, accuracy, and strategy diversity. The quantitative trading system provides these institutions with efficient and scalable solutions, helping them gain a competitive edge in dynamic markets.

Hedge Funds

- Hedge funds use the quantitative trading system for high-frequency trading (HFT), statistical arbitrage, market-neutral strategies, etc., aiming to achieve stable returns in volatile markets.

- The advantages of the quantitative trading system lie in automated trading, quick response to market changes, reduced human decision-making errors, and higher trading frequency and precision.

- Risk Management: The system provides real-time risk value (VaR), conditional risk value (CVaR), and other risk evaluation tools to help hedge funds dynamically adjust their portfolios and avoid potential risks.

Banks and Asset Management Firms

- Banks and asset management firms use the quantitative trading system to optimize portfolio management, asset allocation, and derivatives trading, enhancing asset returns through data-driven decision-making.

- The system's optimization algorithms and deep learning models can extract valuable insights from vast amounts of data, providing market opportunities beyond traditional investment strategies.

- The system also supports multi-asset class investments, helping institutions create returns across stock, bond, futures, and forex markets.

2. Retail Investors

With technological advances, the application of quantitative trading systems is becoming increasingly popular, providing retail investors with customized and intelligent investment tools and platforms. Through robo-advisors and quantitative strategy platforms, retail investors can enjoy professional quantitative investment services, enhancing their market competitiveness.

Robo-Advisors

- Robo-advisor platforms based on the quantitative trading system provide retail investors with automated asset allocation and portfolio management services. By analyzing investors' risk preferences, investment goals, and market data, the platform recommends the most suitable investment strategies.

- The system can adjust portfolio configurations based on real-time market conditions, helping investors maintain stable returns and reduce investment risks in volatile markets.

- Automatic Rebalancing: When significant market changes occur, the robo-advisor can automatically adjust the asset weights in the portfolio, ensuring that risk remains within an acceptable range.

Quantitative Strategy Platforms

- Quantitative strategy platforms allow retail investors to use complex quantitative trading strategies through a simple interface. These platforms provide an open-source strategy library and backtesting tools, helping users validate strategy effectiveness using historical data.

- Strategy Customization: Users can customize trading strategies based on their investment needs and risk preferences, with the platform dynamically adjusting strategies based on real-time data.

- The platform offers strategy evaluation tools to help investors assess the risks and returns of different strategies and optimize their portfolios.

3. API Integration and SaaS Solutions

To facilitate access for various financial institutions and developers, the quantitative trading system offers flexible API integration and SaaS solutions, allowing the system to better integrate with external applications and expand its functionality and application scenarios.

API Integration

- Open API interfaces allow developers and financial institutions to integrate the core functions of the quantitative trading system into existing trading platforms or applications. Through APIs, users can access market data, backtest results, trading signals, and risk management data, as well as implement automated trading using custom algorithms.

- API interfaces provide an efficient integration solution for institutional investors, supporting faster data processing and decision execution.

SaaS Solutions

- The quantitative trading system's SaaS solution allows retail investors and small-to-medium institutions to access advanced quantitative trading technology at a low cost and with minimal barriers. Through SaaS, users can:

- Pay-as-you-go: Pay based on the features used, computing resources, and data storage, providing more flexibility in cost management.

- Cloud Deployment: The system is hosted in the cloud, eliminating the need for users to manage hardware infrastructure, with all computing and data storage managed by the service provider.

- Quick Deployment: Users can quickly begin using the quantitative trading system via SaaS solutions without building infrastructure, improving operational efficiency.

Market Analysis and Future Prospects

With the continuous development of technology, the field of quantitative trading is undergoing unprecedented transformation. This chapter will explore the market position and future development potential of the quantitative trading system through three key aspects: market size and growth trends, competitive analysis, and future technological developments.

1. Market Size and Growth Trends

The market size for quantitative trading systems has seen explosive growth in recent years. With the maturation of artificial intelligence, big data analytics, and machine learning technologies, more financial institutions and retail investors are adopting quantitative trading to improve decision-making efficiency and investment returns.

Market Size

- According to research from MarketsandMarkets, the global quantitative trading market is expected to reach billions of dollars in the coming years. Specifically, AI-driven quantitative trading, as an emerging technology field, is expected to become a significant driver of market growth.

- The application of quantitative trading has expanded beyond traditional stock markets to include futures, forex, and digital currencies. As the market grows, the potential user base for quantitative trading systems is also increasing.

Growth Trends

- AI and Big Data Integration: With the maturity of AI, particularly deep learning and reinforcement learning, the decision-making efficiency and accuracy of quantitative trading systems have significantly improved, providing new growth momentum for the market.

- Retail Investors Rising: Traditionally, quantitative trading has been dominated by institutional investors, but with the popularity of robo-advisors and quantitative strategy platforms, an increasing number of retail investors are participating. This trend injects more vitality into the quantitative trading market.

- Cross-Market Applications: Quantitative trading is no longer limited to the stock market. Investors and trading platforms are increasingly applying quantitative strategies in digital currency markets, forex markets, commodity futures markets, and more.

2. Competitive Analysis

The market for quantitative trading systems is highly competitive, with leading fintech companies, professional quantitative hedge funds, and various technology platforms and service providers as key participants. Companies in the market compete fiercely on technological advantages and market positioning.

Competitive Landscape

- QuantConnect: An open-source quantitative trading platform that supports users in writing and backtesting strategies and provides rich market data. With community-driven development, QuantConnect has become a leading platform in the quantitative trading field.

- Alpaca: Provides quantitative trading API services for retail investors, aiming to provide low-cost, efficient quantitative trading solutions. With its simple interface and powerful features, Alpaca has attracted many developers and retail investors.

- Two Sigma & Renaissance Technologies: As global leaders in quantitative hedge funds, these companies use cutting-edge machine learning and data analytics technologies to predict markets and execute trades, representing the high-end level of institutional quantitative trading.

Advantages and Disadvantages Comparison

-

Our Advantages:

- Technological Innovation: Through advanced AI trading models, deep learning, and reinforcement learning, our quantitative trading system has significant advantages in decision-making speed and accuracy.

- Multi-Market Support: Our system supports multiple financial markets, including the stock market, forex market, futures market, and digital currency market, enabling investors to invest across markets from a single platform.

- API and SaaS Solutions: We offer flexible access options, providing solutions that cater to the needs of both institutional and retail investors.

-

Our Disadvantages:

- Brand Recognition: Compared to market giants like Two Sigma and Renaissance Technologies, our brand has lower market recognition and requires more marketing efforts and customer outreach.

- Initial Investment and Resource Commitment: Although our system features advanced functionality, due to a long development cycle and substantial initial resource investment, it may take some time to see returns.

3. Future Technological Development Directions

With ongoing technological advancements, quantitative trading systems will continue to innovate. Below are the future technological development directions we foresee, which will drive further growth in the quantitative trading industry.

AutoML (Automated Machine Learning)

- AutoML technology aims to automate the selection, training, and optimization of machine learning models, lowering the technical barriers for users of quantitative trading systems. Investors will be able to design and optimize trading strategies using powerful AI technologies without delving into machine learning details.

- As AutoML platforms evolve, users will be able to automatically generate quantitative strategies that match their risk preferences, improving decision-making efficiency for market participants.

AI Agents

- AI agents are autonomous decision-making entities capable of monitoring market changes and executing trading strategies without human intervention. In the future, AI agents will expand beyond trading to include risk management, market forecasting, and portfolio optimization, helping investors comprehensively optimize asset management.

- Adaptability: AI agents will be able to dynamically adjust strategies based on market fluctuations and external changes, ensuring optimal performance in complex market environments.

Quantum Computing in Finance

- The development of quantum computing, particularly advances in quantum algorithms and quantum accelerators, will bring revolutionary changes to the financial sector. Quantum computing can solve complex problems that traditional computers cannot, particularly in optimization, big data analysis, and Monte Carlo simulations.

- In quantitative trading, quantum computing could significantly speed up risk analysis, asset allocation, and high-frequency trading algorithm execution, offering more efficient solutions for investors.

Conclusion and Outlook

In the field of quantitative trading, technological innovation is driving the transformation of the industry. This chapter will summarize the key innovations of the quantitative trading system, its impact on the industry, long-term vision, and future development plans. Through this section, we aim to demonstrate the unique value and future direction of the system.

1. System Innovation Highlights

As an advanced technology, the quantitative trading system injects new vitality into traditional financial markets. Its innovations are reflected in the following aspects:

High-Frequency Trading (HFT)

-

Technological Innovations

- AI-driven Trading Models: The system integrates deep learning, reinforcement learning, and supervised learning, showcasing outstanding accuracy and real-time responsiveness in generating trading signals, market forecasting, and decision execution.

- Multi-market Support: Unlike traditional investment strategies focused on a single market, our system supports joint investments across multiple asset classes, including stocks, forex, futures, and digital currencies, providing global asset allocation for users.

- Adaptability and Automation: By utilizing AutoML and AI agent technologies, the system autonomously generates and optimizes quantitative trading strategies, dynamically adjusting portfolios based on market changes, reducing manual intervention risks, and improving decision-making efficiency.

-

Functional Innovations

- Intelligent Risk Control: The system incorporates real-time risk management and quantitative indicators, monitoring market volatility and automatically executing stop-loss and take-profit strategies to safeguard user assets.

- Optimized Trade Execution: Leveraging an intelligent execution engine, the system dynamically adjusts trading execution methods based on market liquidity and order book information, reducing slippage and transaction costs while improving trading efficiency.

- Interpretability and Transparency: By introducing interpretability methods like SHAP and LIME, investors can understand the decision-making processes of AI models, enhancing trust and usability.

2. Industry Impact and Long-Term Vision

The quantitative trading system is not only a product of technological innovation but also has a profound impact on the entire financial industry, transforming traditional investment models and driving the continuous development of financial technology.

-

Industry Impact

- Improved Market Efficiency: Through data-driven decision-making and real-time automated execution, the quantitative trading system significantly increases market liquidity, reduces human error, accelerates capital flow, and enhances overall market efficiency.

- Popularization of Quantitative Investing: As quantitative trading technology becomes more widely used, an increasing number of investors will be able to use robo-advisors and quantitative strategy platforms, making financial markets more accessible and moving beyond the professional domain of institutional investors.

- Promotion of Financial Product Innovation: As quantitative trading technology advances, more innovative financial products (such as quantitative hedge funds and digital asset management platforms) will emerge, further enriching market options and driving industry innovation and development.

-

Long-Term Vision

- Global Intelligent Investment Platform: Our long-term vision is to create a world-leading intelligent investment platform that provides one-stop solutions across different markets and asset classes. We plan to expand the platform into more countries and regions, serving global investors.

- Comprehensive Digitalization of Financial Markets: With the deepening application of quantum computing, big data analytics, and blockchain technologies, our goal is to bring financial markets into a smarter, more transparent, and efficient era through continuous system optimization.

- Inclusive Finance: In the future, the quantitative trading system will not only serve large institutional investors but also lower the technical barriers for individual investors through SaaS and API interfaces, allowing them to benefit from the advantages of quantitative trading, thus contributing to the development of inclusive finance.

3. Next Steps

To ensure the quantitative trading system achieves its innovative goals and addresses industry challenges, we have formulated a clear next-step development plan:

-

Technical Upgrades and Optimization

- Ongoing AI Model Optimization: We will continue to optimize the AI trading models within the quantitative trading system, exploring additional market signals and enhancing prediction accuracy and real-time responsiveness.

- Integration of Quantum Computing: To improve computational efficiency and optimization capabilities, we plan to integrate quantum computing technology into future versions, especially in areas such as risk management and asset allocation, further enhancing the system's computational power and decision-making ability.

-

Market Expansion and Partnerships

- Global Market Expansion: We will expand our market coverage, particularly in emerging markets such as Asia and Europe, to meet the growing demand from investors. At the same time, we will actively seek partnerships with major financial institutions, hedge funds, and asset management companies to promote deep integration and win-win cooperation.

- Strategic Partnerships: We will establish in-depth partnerships with fintech companies and cloud service providers to create a more stable, convenient, and flexible trading platform, strengthening our market competitiveness through collaboration.

-

Compliance and Security Enhancements

- Adherence to Global Regulatory Standards: We will continue to monitor global financial regulatory requirements to ensure the system is compliant across the world, meeting the standards of agencies such as the SEC, MiFID II, and the China Securities Regulatory Commission.

- Enhanced Data Security: We will strengthen data encryption and privacy protection measures, improving platform security and preventing potential cybersecurity threats and data breaches.

Appendix

This appendix provides supplemental materials related to the quantitative trading system, including terminology explanations, related literature and research papers, and open-source resources and tools to help readers deepen their understanding of the technical concepts and background discussed in this paper. This section serves as a resource for further study and research.

1. Glossary

Many technical terms were used in the development and application of the quantitative trading system. This section provides brief explanations of key terms to help readers better understand the technical content.

- Quantitative Trading: The process of making trading decisions using mathematical models, statistical analysis, and computer programs. Quantitative trading generates trading signals by analyzing historical data and automatically executing trading strategies.

- AI (Artificial Intelligence): A computer system that simulates human intelligence, capable of learning, reasoning, planning, and decision-making. In quantitative trading, AI is used to analyze market data, generate trading strategies, and automatically adjust strategies based on market changes.

- Deep Learning: A machine learning method that uses multi-layer neural networks for data modeling, especially suited for learning and pattern recognition in large datasets. Deep learning is commonly used in quantitative trading for price prediction and signal generation.

- Reinforcement Learning: A machine learning method where an agent learns actions through interaction with the environment to maximize cumulative rewards. In quantitative trading, reinforcement learning is used to develop self-optimizing trading strategies.

- Backtesting: The process of testing a quantitative trading strategy on historical data to evaluate its effectiveness. Backtesting helps verify whether a strategy would have achieved the desired returns under past market conditions.

- VaR (Value at Risk): A risk management technique used to assess the maximum potential loss a portfolio might incur over a specified time period with a given confidence level.

- API (Application Programming Interface): The interface through which different software components communicate with each other. In quantitative trading systems, APIs allow users to integrate trading strategies with the platform.

- AutoML (Automated Machine Learning): The automation of the machine learning process, designed to simplify model selection, training, and optimization, reducing the barriers to using machine learning.

- Quantum Computing: A computing method based on quantum mechanics principles that can efficiently solve complex problems traditional computers cannot handle. Quantum computing may be applied in quantitative trading for optimization, data processing, and simulation.

2. Related Literature and Research Papers

The following is a list of referenced literature and research papers cited in this article. Readers can refer to these resources for further in-depth understanding of quantitative trading, AI technology, machine learning algorithms, and their applications in financial markets.

1. Chan, E. (2009). Quantitative Trading: How to Build Your Own Algorithmic Trading Business. Wiley.

This book introduces the basic concepts of quantitative trading and how to build an algorithmic trading system, a classic work in the field of quantitative trading.

2. He, K., Zhang, X., Ren, S., & Sun, J. (2015). Delving Deep into Rectified Linear Units: Beyond Human-Level ImageNet Classification. arXiv preprint arXiv:1502.01852.

This paper introduces the innovation of the ReLU activation function and proposes a new deep learning network architecture, laying the foundation for the application of deep learning in financial markets.

3. Silver, D., Huang, A., Maddison, C. J., et al. (2016). Mastering the Game of Go with Deep Neural Networks and Tree Search. Nature, 529(7587), 484-489.

This paper demonstrates the application of deep reinforcement learning in complex decision-making problems, especially the success of AlphaGo in Go, providing theoretical support for reinforcement learning in quantitative trading.

4. Jarrow, R. A., & Protter, P. (2004). A New Derivatives Pricing and Modeling Approach. International Journal of Theoretical and Applied Finance, 7(3), 421-445.

This paper proposes a quantitative model for derivatives pricing and provides commonly used pricing methods and risk management techniques in quantitative trading.

5. Feng, Y., & Lee, C. M. (2020). Machine Learning in Financial Markets: A Survey. arXiv preprint arXiv:2002.00819.

This paper surveys the application of machine learning in financial markets, covering model building, algorithm selection, and risk management, providing valuable references for financial professionals.